Not every investor sets out to beat the market. Some want stable cash flow with low volatility, especially as they get closer to retirement. Income funds can help with that transition. Instead of juggling individual stocks, earnings reports and market headlines, investors can rely on a single fund that packages dozens or even hundreds of income?producing securities together.

Of course, not all income funds are created equal. These strategies rarely outperform the S&P 500 over long periods, but the goal isn’t market?beating returns – it’s generating consistent income with a smoother ride. Some funds lean on high?dividend stocks or high-yield bonds, while others use covered calls to boost cash flow.

It’s important to analyze the quality, sustainability, diversification and costs of the funds you consider, says Daniel Milan, investment advisor representative and managing partner at Cornerstone Financial Services in Southfield, Michigan. Assess the fund’s distribution track record and “look under the hood” to ensure the underlying holdings meet your quality standards. The expense ratio also directly affects your returns as every cent that goes toward covering fund costs is not going toward generating returns.

What Are Income Funds?

Income funds typically hold dividend?paying stocks, bonds, or a mix of both, giving investors built?in diversification and a more predictable stream of income through interest and dividends. Many of the underlying holdings are established, blue?chip companies that tend to be less volatile than fast?growing names. That stability can be especially appealing for retirees who want to avoid sharp, unexpected drawdowns.

Why Investors Buy Income Funds

These funds don’t generate the highest returns you can get, and the distributions are often subject to tax. If you aren’t retiring anytime soon, you can reinvest dividends back into the fund to grow your holdings. Accumulating more shares now will result in higher payouts in the future. You will then have more choices in retirement, especially if you have other income sources like Social Security.

Conversely, if you are in your distribution or retirement years, “income funds are able to provide a more stable or predictable cash flow projection over the long term,” Milan says.

While many investors can benefit from allocating a percentage of their portfolio to income funds, it’s important to choose the right funds for your portfolio. Below are some of the top income funds to consider, all of which have a balance of solid ratings, decent to high yields and good long-term returns. Each has a different risk-return profile, though, so don’t just grab the highest-yielding fund without ensuring you’re comfortable with the risk.

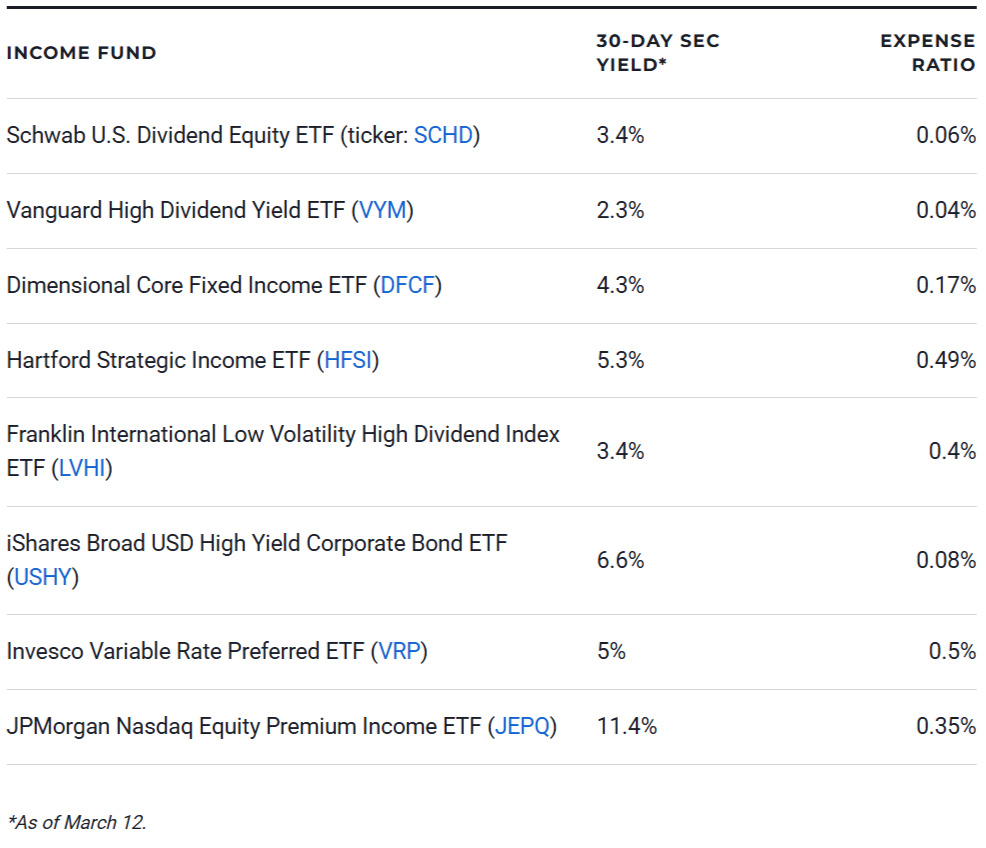

INCOME FUND

Schwab U.S. Dividend Equity ETF (ticker: SCHD)

Vanguard High Dividend Yield ETF (VYM)

Dimensional Core Fixed Income ETF (DFCF)

Hartford Strategic Income ETF (HFSI)

Franklin International Low Volatility High Dividend Index ETF (LVHI)

iShares Broad USD High Yield Corporate Bond ETF (USHY)

Invesco Variable Rate Preferred ETF (VRP)

JPMorgan Nasdaq Equity Premium Income ETF (JEPQ)

Schwab U.S. Dividend Equity ETF (SCHD)

The Schwab U.S. Dividend Equity ETF is one of the most well-known high-yield ETFs. It has more than $84 billion in net assets and a 0.06% expense ratio that blows away most of the competition. With a 3.4% SEC yield from a quarterly dividend payment and an annualized 9.5% return over the past five years, it’s easy to see why many investors love this income fund.

The fund’s top three holdings are Lockheed Martin Corp. (LMT), ConocoPhillips (COP) and Verizon Communications Inc. (VZ), which make up more than 14% of the fund’s total assets. The top 10 holdings attract 42% of SCHD’s assets, and there’s a strong focus on energy, consumer defensive and health care stocks.

Vanguard High Dividend Yield ETF (VYM)

Vanguard funds are known for lower expense ratios than average, and this no-load fund is no exception. The Vanguard High Dividend Yield ETF undercuts SCHD with a 0.04% expense ratio, but slightly lower 30-day SEC yield. The fund has $92.3 billion in assets under management, spread across 562 stocks.

Unlike SCHD, VYM leans primarily on financial and technology companies, at nearly 21% and over 16% of the portfolio, respectively. The top three VYM holdings are Broadcom (AVGO), JPMorgan Chase & Co. (JPM) and Exxon Mobil Corp. (XOM), which make up about 13.3% of the portfolio. Roughly one-quarter of the fund’s assets are in the top 10 holdings.

VYM pays out a quarterly dividend and has a 30-day SEC yield of 2.3%. The fund has a 11.3% annualized return over the past five years as of March 12.

Dimensional Core Fixed Income ETF (DFCF)

Dividend stocks are one way to generate income, but they aren’t the only option. Bond funds can generate even more reliable income, although this often comes at the expense of lower capital appreciation. DFCF hasn’t turned five yet – the fund launched in November 2021 – but it returned just over 5.8% over the past three years. Not too shabby for a bond fund, especially when paired with a 4.3% 30-day SEC yield paid through a monthly distribution and a 0.17% expense ratio.

It invests in over 1,600 U.S. and foreign investment-grade fixed-income securities. It currently holds a fairly even split between government and corporate securities (37% and 39% of the portfolio, respectively) with another 21% in securitized assets, like agency mortgage-backed securities. In fact, the top three holdings are mortgage-backed securities guaranteed by Fannie Mae. The average credit rating is A+, so you’re in fairly secure hands here.

Hartford Strategic Income ETF (HFSI)

If you want more income potential than a traditional core bond fund typically provides, HFSI may be for you. Instead of sticking to one corner of the fixed-income market, HFSI takes a multi-sector approach, mixing high?yield bonds, emerging?markets debt, bank loans and securitized credit. That flexibility gives the fund room to seek attractive yields across changing market environments while managing risk through broad diversification.

This approach can also give it a stronger income profile, but potentially more volatility, too. However, as of the time of this writing, HFSI has a standard deviation of 5 compared to 5.25 for DFCF. HFSI also captures more upside and considerably less downside than DFCF. Where HFSI falls behind is in its expense ratio, which sits at 0.49%. For this, you get a 30-day SEC yield of nearly 5.3% and a three-year annualized return of 8.1% as of March 12.

Franklin International Low Volatility High Dividend Index ETF (LVHI)

Global diversification is important, even in your income portfolio. LVHI is designed for investors who want reliable income from overseas markets without taking the full swings of international stocks. It targets high-quality companies that pay “healthy and sustainable dividends” while focusing on low volatility.

It mitigates exchange rate risk with a currency hedge strategy. This strategy means the fund will likely have higher returns than an equivalent unhedged fund when the U.S. dollar is strengthening, and lower comparable returns when the U.S. dollar is weakening.

The fund can hold anywhere from 50 to 200 securities, though the number may vary due to market conditions. LVHI currently sits at 211 securities, including 191 stocks. These come from 20 countries, spanning continents from Australia to Europe and Asia. It pays a quarterly dividend with a 3.4% 30-day SEC yield and has returned an annualized 16.4% over the past five years.

iShares Broad USD High Yield Corporate Bond ETF (USHY)

The iShares Broad USD High Yield Corporate Bond ETF has one of the most impressive expense-to-yield pairings on this list. With a 0.08% annual expense ratio and 6.6% 30-day SEC yield, this one is hard to beat.

The fund gives a simple, low-cost way to tap into the income potential of the U.S. high-yield bond market. USHY tracks a broad index that includes nearly 2,000 below-investment grade bonds. This diversification is key when you’re dealing in the junk bond market where defaults are more likely. Only 3% of the fund’s assets are in the top 10 names, and none account for more than 0.46% of the portfolio.

As a fixed-income fund, you won’t get the capital appreciation of equity funds. USHY returned an average of about 4.3% over the past five years. But in exchange, you get more stable income and lower volatility.

Invesco Variable Rate Preferred ETF (VRP)

The trouble with common dividend stocks is that dividends are not guaranteed. A company can cut or reduce its payout at any time. One way to minimize the chance of your income being cut at the whim of company management is to invest higher up the capital structure. Enter: preferred stocks.

Preferred shareholders have a higher claim to company assets than common shareholders. In other words, companies must pay preferred dividends before they pay common dividends. This priority in the pecking order makes preferred income more stable than equity-only funds, especially during periods of corporate stress when dividend cuts become more common. VRP adds an extra layer of security by diversifying across banks, insurers, utilities and other preferred-heavy industries.

VRP holds variable-rate preferred stocks whose coupons reset as interest rates change. As such, it can help you maintain income even when interest rates are rising, a scenario that often pressures both bonds and high-dividend equities.

VRP isn’t necessarily a substitute for a more traditional income fund like others on this list, but rather a good complement. Adding a variable rate preferred fund can broaden your income sources and reduce your reliance on equity markets alone. It boasts a 5% 30-day SEC yield and pays a monthly dividend. However, since preferreds sit between common equity and bonds, the annual return on these funds is a bit lower. VRP returned an annualized 4.6% over the past five years.

JPMorgan Nasdaq Equity Premium Income ETF (JEPQ)

Now for the real yield powerhouse on this list: JEPQ. With an 11.4% 30-day SEC yield delivered through monthly distributions, your income stream will be fat and happy with this one. What’s more, the fund returned an annualized 23.4% over the past three years. It launched in May 2022, so five-year performance isn’t available yet.

It pulls these impressive stats off by applying fundamental data science to select companies from the Nasdaq-100 index, which holds nonfinancial companies listed on the Nasdaq stock market. /It pairs this equity portfolio with a derivatives strategy of writing out-of-the-money call options on the Nasdaq-100 index to generate additional income through the premiums collected. By trading a portion of its upside potential in exchange for options premiums – the call options will be exercised if the stocks appreciate above the strike price – JEPQ can deliver a slightly smoother ride.

For income?focused investors looking to diversify beyond bonds and dividend stocks, JEPQ offers a practical way to earn higher payouts from one of the market’s most dynamic sectors, without relying solely on price appreciation.