The two “I’s” – Iran and innovation – continue to define the global drone market, which is expected to grow from $69 billion in 2026 to $147.8 billion in 2036, according to technology research firm IDTechEx. That represents a compound annual growth rate, or CAGR, of 7.9%.

“Commercial deployments are accelerating rapidly, with unit shipments expected to surpass 9 million in 2036,” the firm says. “This growth reflects increasing regulatory clarity, maturing technology stacks, falling hardware costs and the transition toward autonomous, data-driven operations.”

Industry observers say the drone industry has been getting lots of attention recently due to military applications, especially with the media coverage of drone attacks in the U.S.-Iran and Russia-Ukraine wars.

“It’s mostly consumer first-person-view (FPV) drones that are used day-to-day in Iran, while larger UAV machines are also at play, which is a fairly different segment,” says Richard Demeny, founder and chief technology officer at Canary Wharfian, a London-based investment banking platform.

For example, Shenzhen, China-based Da-Jiang Innovations, a drone market leader, did not receive a mandated U.S. security clearance by the end of 2025, which led to a Federal Communications Commission ban on new import authorizations due to national security risks. “This scenario has drone service providers scrambling for NDAA-compliant, non-Chinese alternatives like Skydio, Teledyne FLIR SIRAS, Freefly, Inspired Flight and Anzu Robotics,” Demeny says. “However, these options are quite expensive, costing $10,000 to $30,000 per unit versus DJI’s sub-$5,000 models that are best for mapping purposes and marketing.”

That reality creates a massive market gap for budget-friendly Western-made drones and presents a good long-term buying opportunity, Demeny notes. Operational and logistical factors should also be considered in any potentially large-scale investment in the drone industry.

“The defining issue impacting drone development in 2026 is production scalability versus supply-chain fragility,” says Brian Chee, founder of Moorpark, California-based BJC Logistics, which specializes in defense and aerospace logistics. “Designing a high-performance drone is no longer the hardest part; securing the microelectronics, raw materials and manufacturing capacity to build tens of thousands of them is the main challenge.”

Thus, the demand for drones is much higher than that for other weapons. “That’s because drones require a lot more advanced materials and are typically unrecoverable when destroyed,” Chee says.

Given the higher demand for drone technologies in 2026, some investors may opt to overlook operational and logistical risks the industry is seeing right now and go where the money is. That means picking industry winners in a fast-moving market that favors innovative drone companies that have a demonstrated track record of performance. That list could include the following drone industry names:

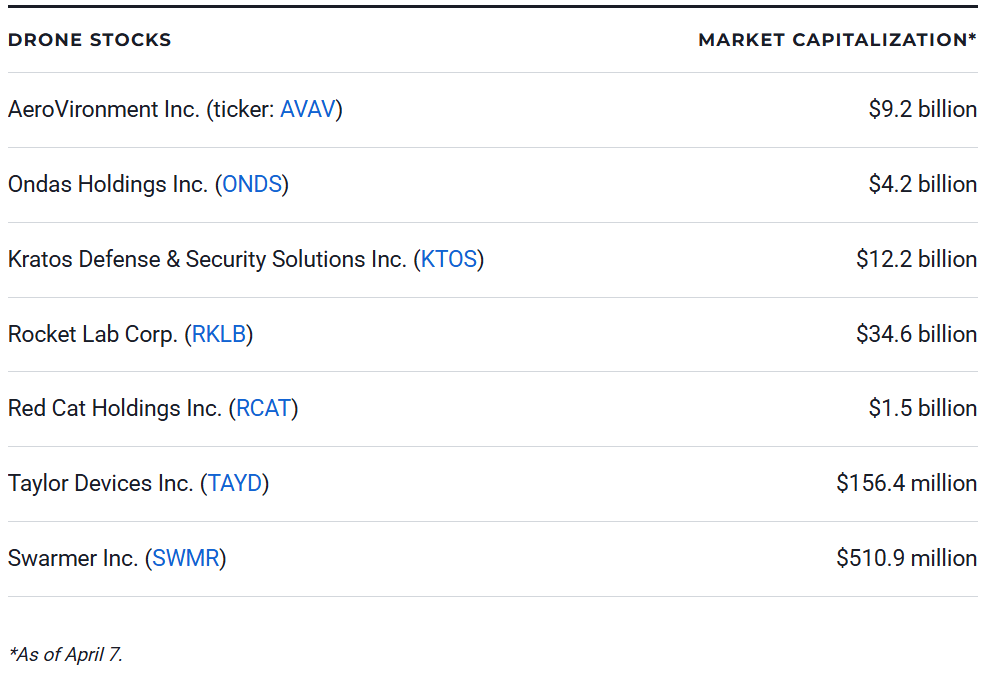

DRONE STOCKS

AeroVironment Inc. (ticker: AVAV)

Ondas Holdings Inc. (ONDS)

Kratos Defense & Security Solutions Inc. (KTOS)

Rocket Lab Corp. (RKLB)

Red Cat Holdings Inc. (RCAT)

Taylor Devices Inc. (TAYD)

Swarmer Inc. (SWMR)

AeroVironment Inc. (AVAV)

AVAV’s great run has come to a skidding stop, with the stock down over 40% in the past three months and down 17.6% in the last month. Like many market plunges, AVAV’s freefall wasn’t attributed to a single issue. Instead, it fell victim to weak quarterly earnings and the loss of a $1.7 billion drone contract with the U.S. Space Force. That fueled a reassessment of AVAV shares by company management, with AeroVironment’s full-year revenue guidance now standing at $1.85 billion to $1.95 billion, down from $1.95 billion to $2 billion, with most fingers pointing to the abandoned Space Force deal.

Still, market trackers support a company comeback, with some calling AeroVironment the gold standard for tactical, combat-proven drones. “Their Switchblade loitering munitions are in incredibly high demand, and they are sitting on a massive, billion-dollar-plus funded backlog,” Chee says. “They have the government relationships and the operational scale to execute.”

Ondas Holdings Inc. (ONDS)

At a price around $9 and with its shares down 26% over the past 90 days, this West Palm Beach, Florida-based wireless radio systems company’s stock has been volatile. It develops unmanned aircraft systems (UAS) and secure private wireless networking systems, primarily in the U.S., Israel and India.

Ondas is moving aggressively across multiple drone fronts, landing a $21 million contract as a strategic investor with the U.S. Army to support C100 UAS and multi-mission payloads. Additionally, a merger with Bethesda, Maryland-based Mistral Group, an assembly and integration systems company with deep ties to government contractors, especially in key areas like defense and public safety, gives ONDS another boost.

The company’s share slide seems at odds with analyst sentiment on the stock, which is trending positive. Take Amit Dayal of H.C. Wainwright, who held a $25 price target in late March, pointing to a big order backlog and 50%-plus gross margin estimates. Ondas is “entering 2026 from a position of strength in the autonomous aerial and robotics markets with a sales pipeline of over $500 million and multiple active M&A targets,” Dayal notes.

Both Needham (a $23 price target) and Maxim Group ($22) followed suit, lending credence to the notion that it’s a smart “buy at the dip” prospect right now.

Kratos Defense & Security Solutions Inc. (KTOS)

Kratos, a recent addition to the S&P SmallCap 600 Index, has suffered the same fate as its drone-industry peers, with its share price down 14.8% over the past month. Company shares rebounded in early April, with shares popping 10% following a key “buy” call on KTOS from Jefferies, which maintained a price target of $85, representing a 26% pop from its current trading levels. Jefferies is hardly alone. Nine of 11 technology analysts rate KTOS a “buy,” with a consensus 12-month price target implying 58% share-price growth.

Kratos, with $1 billion in annual revenue from its advanced-tech tactical drones and electronic warfare solutions, recently reported Q4 results that beat Wall Street revenue expectations, recording sales up 22% year over year to $345.1 million.

Wall Street veterans point to the company’s jet-powered combat drones as an important reason to buy, with the XQ-58 Valkyrie becoming a formal Program of Record under a $231.5 million Marine Corps contract in January. “The company also manufactures the turbine engines that go into other companies’ drones, so it is both a platform builder and a picks-and-shovels supplier,” says Kunal Desai, founder of Bulls on Wall Street Revenue, an investment trading educational company. “Guidance is $1.6 billion for 2026.”

Rocket Lab Corp. (RKLB)

Long Beach, California-based Rocket Lab is trading around $64 per share and down over 21% for the last three months, as of the first week of April. RKLB is another example of a company caught in the tech-stock quagmire of 2026.

Yet the company’s prospects are solid, as it is likely to be a major beneficiary of President Donald Trump’s call for a $1.5 trillion defense budget in 2027, up 42% from 2026 if the number sticks. Rocket Lab’s shares rose over 5% on news of the Trump defense budget, and it should be seen as a big performance booster for the stock going forward.

The company, which develops spacecraft and systems and provides launch services for government and commercial customers, is unique in the drone industry because it doesn’t produce pure drones; instead, it builds reusable orbital rockets. Its flagship Electron has 81 launches under its belt and has deployed 248 space satellites. The company’s next spacecraft, Neutron, is set to launch in late 2026 and is expected to haul more substantial payloads, up to 40 times its current capacity.

The company was also buoyed with a March 18 announcement of a $190 million contract to conduct 20 hypersonic flight tests with its HASTE launch vehicle for the U.S. Defense Department, signaling its tightening ties to the government.

“The new award is the single-largest launch contract in Rocket Lab’s history, bringing the total number of launches in backlog to more than 70 and pushing Rocket Lab’s total backlog across launch and space systems to more than $2 billion,” the company says.

Red Cat Holdings Inc. (RCAT)

While this San Juan, Puerto Rico-based drone services company did see its share price decline by 15% over the past month, it’s still up 21% over the past three months and up 65% year to date. RCAT specializes in software systems for drones and other robotics products. Its navigation and mapping business provides imaging tools to collect detailed location and mapping data. The company also develops systems that plan and control flight operations and analyze data in real time.

The company saw an immediate 20% boost in its shares immediately after the joint U.S.-Israel military strike on Iran in late February, as the operation relied heavily on one-way unmanned attack drones to take out Iran’s nuclear arsenal, which turned investor attention to drone providers like Red Cat. Investors had already expressed burgeoning interest in Red Cat’s international business, particularly as NATO allies ramped up spending. In late 2025, the company’s Red Cat Holdings subsidiary, Teal Drones, received the green light to have its Black Widow small unmanned aircraft systems installed in the NATO Support and Procurement Catalog, allowing NATO members to purchase access to the system.

RCAT seems like it will continue to prime the market pump, strengthened by a slew of Black Widow drone contracts and a new deal with an as-yet-unnamed NATO country to supply small military drone systems, with delivery pegged for the end of the year.

Wall Street likes where RCAT is positioned, with sector analysts calling for a consensus $20.67 price target, representing a roughly 67% potential upside.

Taylor Devices Inc. (TAYD)

Trading at $50 per share but down 39% over the past month, this North Tonawanda, New York-based company specializes in the design, development, manufacture and marketing of shock-absorption, rate-control and energy-storage devices.

The company’s Q3 2026 earnings report held up well, with earnings per share up to 79 cents, easily beating the 64 cents in the prior-year quarter. Net sales were up, too, at $11.2 million, up from $10.6 million a year ago. Net income was up 25% as well, while cash flow landed at $7.1 million, up from $5.5 million a year ago, with management pointing to more robust net income and larger sales to aerospace and defense customers. Overall, Taylor’s improving financial picture should give investors a good reason to get in at low levels on TAYD shares.

“TAYD has no debt and a ton of cash on the balance sheet,” says Peter Sanchez Guarda, a financial derivatives attorney at TurnKey Family Office in Washington, D.C. “They make landing gear for Reaper and Predator drones, as well as their other businesses, like earthquake dampers for buildings.”

Swarmer Inc. (SWMR)

Swarmer, which went public on March 17, saw its share price rise from $5 to $31 on day one, a 520% increase, enabling the Austin, Texas-based company to raise about $15 million through the sale of 3 million shares. The share price almost doubled on the second day of trading, up almost 1,100% for the two-day trading period.

Why the interest in a highly speculative company with a grand total of $310,000 in revenues last year? Potential, market watchers say.

Swarmer is a “speculative momentum name,” Desai says. “Its AI-powered software lets one operator control a swarm of drones, and the technology has been battle-tested in Ukraine with 100,000 missions.”

Despite its paltry revenue history, Swarmer has a $33 million backlog and targets $20 million in 2026 revenue, but at current prices, the valuation is completely detached from fundamentals. “If you trade this, you’re trading the narrative, not the business, so size accordingly,” Desai adds.

One Strategy Shift to Make on Drone Stocks Right Now

Market watchers advise investors not to get too focused on artificial intelligence plays in lieu of solid industries like drones, noting there are more opportunities missed than gained in doing so.

“Investors are largely missing the boat on drones because they’re artificially separating AI from hardware,” Chee says. “The current market frenzy has concentrated capital into large language models and silicon (like Nvidia), leaving drone stocks overlooked.”

Chee notes that AI requires a physical vessel to execute actions in the real world, and the drone industry is a good example. “The most significant leap in defense technology right now isn’t just a smarter algorithm or code; it’s AI-enabled swarming, autonomous targeting and navigation in GPS-denied environments,” he says. “Investors who only buy software stocks are missing out on the companies actually deploying that AI onto the battlefield and into industrial infrastructure.”